Bad Debt Analysis for a Construction Material Distributor

Reduced write-offs by 28% within 9 months through proactive intervention.

Client Context

A regional construction material distributor supplying cement, aggregates, steel, and finishing products to contractors, developers, and retailers faced a persistent rise in bad debt and overdue receivables.

Despite strong sales growth, profit margins were eroding due to credit losses and inefficient collections.

The company operated across multiple customer segments—B2B, wholesalers, and retail—and extended trade credit with limited visibility into risk patterns or repayment behavior.

Leadership sought a data-driven approach to analyze, predict, and reduce bad debt exposure while maintaining sales competitiveness.

Key Challenges

Rising Credit Losses: Bad debt increased by 40% year-over-year, largely driven by a few high-value construction clients.

Weak Credit Scoring Practices: Credit approvals were based on manual judgment and outdated financial data.

Fragmented Receivables Data: Customer payment histories were scattered across legacy ERP systems and regional ledgers.

Poor Predictive Insight: No early-warning mechanism existed to identify at-risk accounts or detect deteriorating credit behavior.

Collections Inefficiency: Field teams lacked prioritization, often pursuing low-risk customers while high-risk debts aged further.

Solution Design

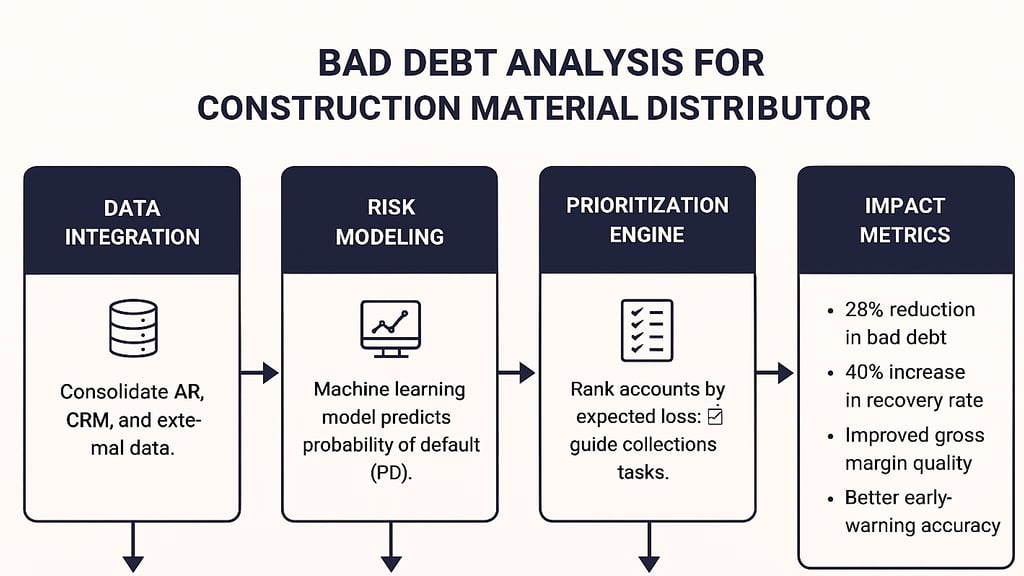

Hal Praxis implemented a Bad Debt Analytics Framework that integrated financial, behavioral, and external credit data to identify risk patterns, predict defaults, and guide collections prioritization.

Key Components

Data Consolidation Layer

Integrated AR data from ERP, CRM, and regional accounting systems into a centralized data warehouse.

Cleaned and standardized customer, invoice, and payment data across 8,000 accounts and 3 years of transactions.

Credit Behavior Profiling

Segmented customers by business type, size, payment behavior, and historical default rate.

Derived behavioral indicators such as average delay days, partial payment frequency, and dispute ratio.

Machine Learning Risk Scoring

Developed ML models (logistic regression and XGBoost) predicting probability of default (PD) based on payment trends, credit terms, and macro factors (construction activity, commodity prices).

Model trained and validated on historical defaults, achieving an AUC of 0.87 in predicting risky accounts.

Collections Prioritization Engine

Ranked receivables by expected loss (PD × exposure × recovery rate) to focus collection efforts on high-impact accounts.

Provided daily collector task lists and performance tracking via dashboards.

Strategic Credit Policy Alignment

Redefined credit limits and payment terms by customer segment and risk class.

Introduced risk-based pricing and credit insurance guidelines for large B2B clients.

Key Deliverables

Bad Debt Analytics Dashboard – interactive visualization of overdue amounts, default trends, and recovery performance.

Customer Risk Scoring Model – ML-driven probability of default (PD) scores with segment benchmarks.

Credit Behavior Report – analysis of payment trends, anomalies, and dispute patterns.

Collections Prioritization Tool – ranking engine for targeted recovery actions by impact potential.

Policy & Governance Framework – credit approval, monitoring, and escalation matrix for sustainable receivables management.

Early Warning Alerts – predictive notifications for accounts showing deteriorating payment behavior.

Business Impact

Bad Debt Reduction: Reduced write-offs by 28% within 9 months through proactive intervention.

Improved Collections Efficiency: Collection teams recovered 40% more overdue amounts per month.

Risk-Adjusted Profitability: Sales decisions integrated credit risk, improving gross margin quality by 3%.

Enhanced Credit Discipline: Credit terms and exposure aligned to customer risk profiles across all regions.

Predictive Control: Early-warning accuracy for at-risk accounts increased from 55% to 89%.

Conclusion

The Bad Debt Analysis & Risk Scoring Model enabled the client to shift from reactive collections to predictive, risk-aware credit management.

By combining behavioral analytics and machine learning, the distributor achieved a sustainable balance between sales growth and credit risk control, ensuring healthier cash flow and stronger financial resilience.

© Hal Praxis 2025. All rights reserved.

Register Code: 304291595

Anapilio 30 Vilnius, Lithuania