Valuation Model for an Electronics Startup

3-year projections to support Series A fund raising.

Client Context

An early-stage electronics technology startup was preparing for institutional fundraising following initial commercial traction. The company operated at the intersection of advanced hardware manufacturing and proprietary technology, with a business model combining product sales, recurring revenues, and long-term scalability potential.

While the leadership team had developed detailed financial projections, they lacked a structured valuation framework that could translate operational assumptions into an investor-credible valuation narrative. Existing analyses were fragmented and did not clearly articulate value drivers, capital requirements, or downside risks.

The objective was to build a robust valuation model that could support investor discussions, scenario analysis, and internal strategic planning.

Key Challenges

Complex Cost and Revenue Dynamics

The business exhibited:

High upfront investment in equipment and R&D

Evolving unit economics as production scaled

Sensitivity to utilization rates, pricing, and cost learning curves

Unclear Link Between Operations and Valuation

While financial forecasts existed, they were not explicitly connected to:

Cash flow generation capacity

Capital intensity and reinvestment needs

Value inflection points tied to scale

This limited management’s ability to justify valuation expectations.

Investor Readiness

The company needed a valuation approach that could:

Withstand financial diligence

Clearly explain assumptions and sensitivities

Be flexibly adjusted for different funding scenarios

Solution Design

A bottom-up valuation model was developed based on the startup’s financial projections and operational assumptions.

Integrated Financial Forecast

The model consolidated:

Revenue projections by product and channel

Cost structure evolution (fixed vs. variable components)

Capital expenditures and working capital requirements

Cash Flow–Driven Valuation Logic

Free cash flows were derived directly from projected performance, enabling:

Discounted cash flow (DCF) valuation

Clear visibility into value creation timelines

Separation of growth value versus operational efficiency gains

Scenario & Sensitivity Analysis

The model allowed management to test:

Different growth and pricing trajectories

Cost optimization and scale-up efficiencies

Funding timing and capital structure impacts

Capital Requirements & Dilution Perspective

The valuation framework incorporated:

Planned funding rounds

Cash runway under alternative scenarios

Implicit dilution effects

Key Deliverables

Startup Valuation Model grounded in detailed financial projections

Scenario & Sensitivity Engine highlighting key value drivers

Investor-Ready Valuation Outputs suitable for pitch decks and discussions

Management Decision Tool for evaluating growth and funding strategies

Business Impact

Clear Valuation Narrative

The startup gained a defensible, transparent valuation story tied directly to operational performance and scalability.

Improved Investor Confidence

The model enabled structured discussions with investors, reducing ambiguity around assumptions and value drivers.

Better Strategic Planning

Leadership could assess how operational decisions—pricing, scaling pace, cost structure—translated into enterprise value.

Funding Readiness

The valuation framework supported capital planning by clarifying funding needs, timing, and dilution implications.

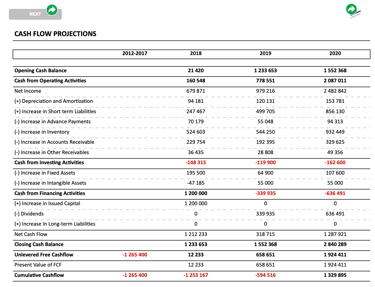

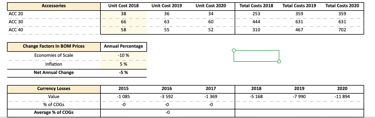

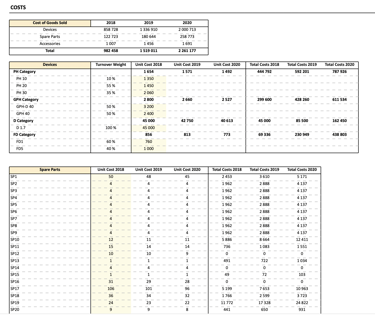

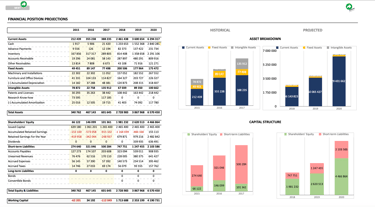

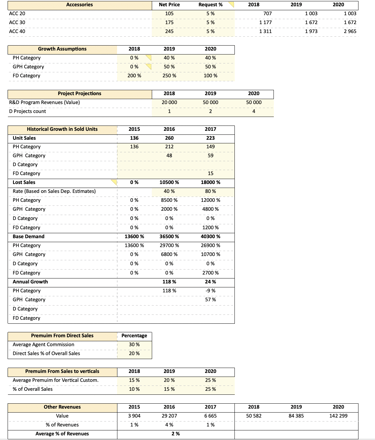

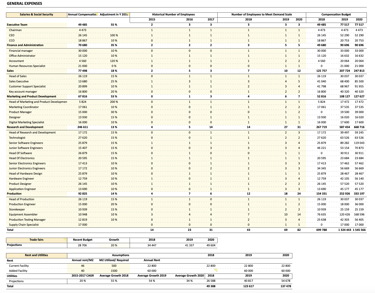

Deliverable Excerpts (Not Exhaustive)

© Hal Praxis 2025. All rights reserved.

Register Code: 304291595

Anapilio 30 Vilnius, Lithuania